| | Good morning, The K-shaped economy isn’t just a theory anymore. After months of “best economy ever” talk, the White House is now starting to acknowledge recession risks, with Treasury Secretary Scott Bessent saying parts of the economy are already contracting. The question is whether he's genuinely concerned or simply nudging the Fed to stick to the plan in December. This week’s earnings could be the clearest test yet of who’s feeling it and who’s not. We’ll hear from McDonald’s, Yum Brands, and Under Armour, a proxy gauge of whether upper-middle-class spending is still carrying the consumer economy while everyone else keeps cutting back. Meanwhile on Wall Street, the AI trade is getting more selective. Palantir’s blowout quarter gave a fresh breath of air, but investors are starting to judge how companies spend, not just how much.

Over in geopolitics, the rare-earths rally just hit a wall. After Trump paused new tariffs and China loosened export controls, markets instantly repriced anything tied to the “permanent trade war” narrative. Let’s dig in. | | | | | Hang tight, Dan Runkevicius, Chief Editor | |  | | | | | “We are seeing, and have been seeing, this divergence in the credit quality, so a flight to both the super prime and to subprime. We’ve seen it going on for a few years now, and now it looks like it’s at a point that it’s substantiating the K-shaped economy.” — TransUnion VP Michele Raneri | | | | | Five things to know before opening bell | | |

🏛️ Shutdown nears record The shutdown, now days away from becoming the longest in U.S. history, is starting to bite. The White House says it will only cover half of this month’s SNAP benefits, leaving 42 million Americans unsure about their next grocery run. A federal judge ordered full payments, but the administration hasn’t agreed to release the funds. And with the holidays kicking in, travelers are about to run into TSA and air-traffic crews working without pay. ⚠️ White House signals recession risk Pundits have been calling a slowdown for months, but now the warning is coming from inside the house. Treasury Secretary Scott Bessent said this week that parts of the economy are already in recession, which is a notable shift from Trump’s “best economy ever” script. 🏦 Fed split on December Chicago Fed’s Austan Goolsbee says he’s “undecided” on another cut, while Mary Daly and Lisa Cook are also sounding cautious. Others argue that stable unemployment and sticky inflation justify holding rates steady. With the final meeting of 2025 approaching, this call may come down to instinct as much as data. 🍟 Earnings to test the consumer split This week’s earnings lineup (McDonald’s, Yum Brands, Under Armour) should show whether the upper-middle class is still doing the heavy lifting for consumer spending. Inflation remains sticky, rates are lower, and the shutdown is a wild card. If management teams start talking about value menus, shrinking traffic, or weaker demand at the margins, it’s another sign the K-shaped divide is widening. 🤖 Palantir keeps the AI trade roaring Palantir kicked off the week with a monster quarter. Revenue is up 63% to $1.18B, government business up 52%, commercial more than doubled. Deals with Nvidia, Snowflake, and Lumen are giving analysts more reasons to stay bullish on the AI trade, but CEO Alex Karp says weaker AI players will “disappear.” | | | | 🤖 AI spending is no longer impressing everyone

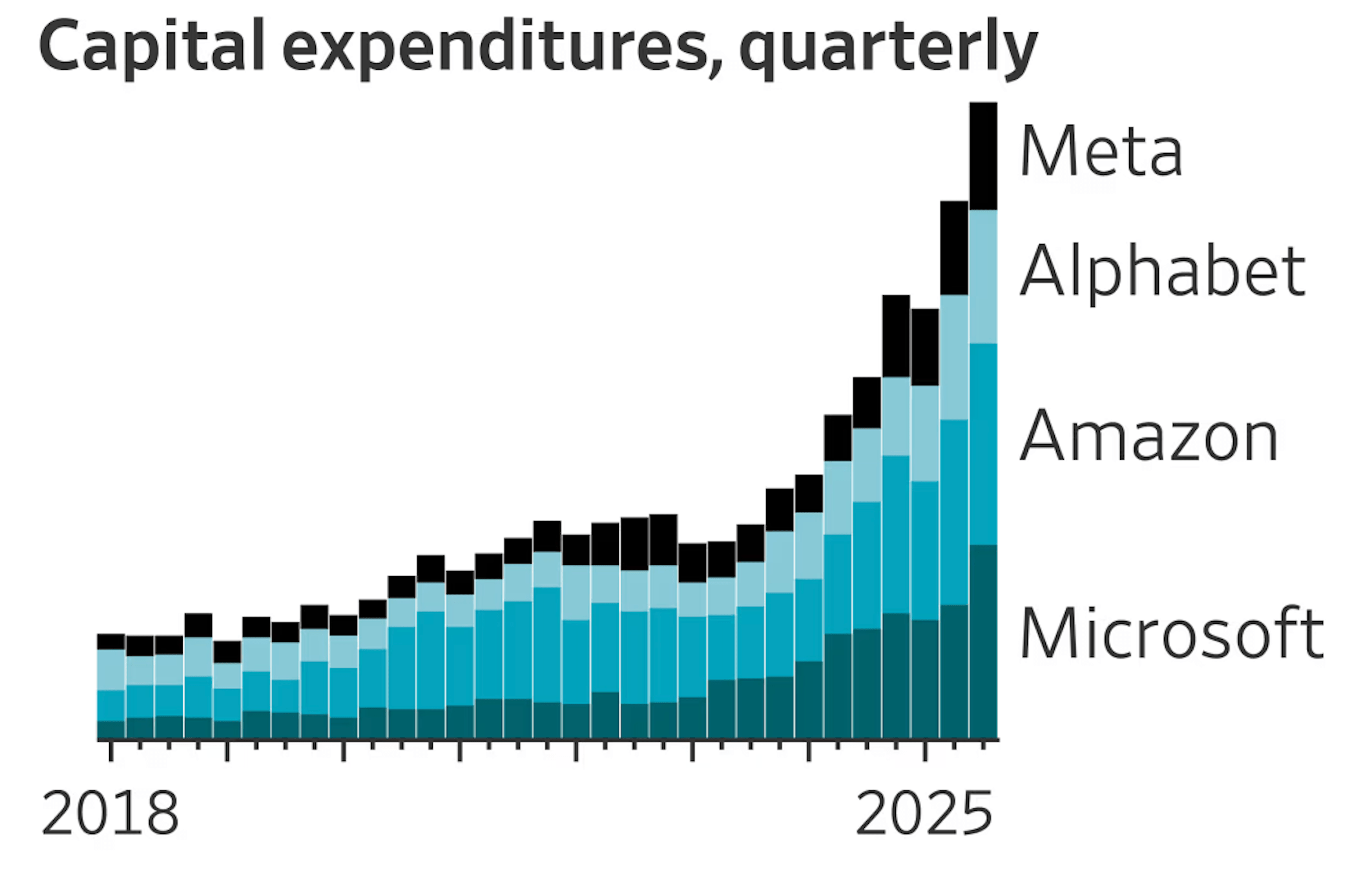

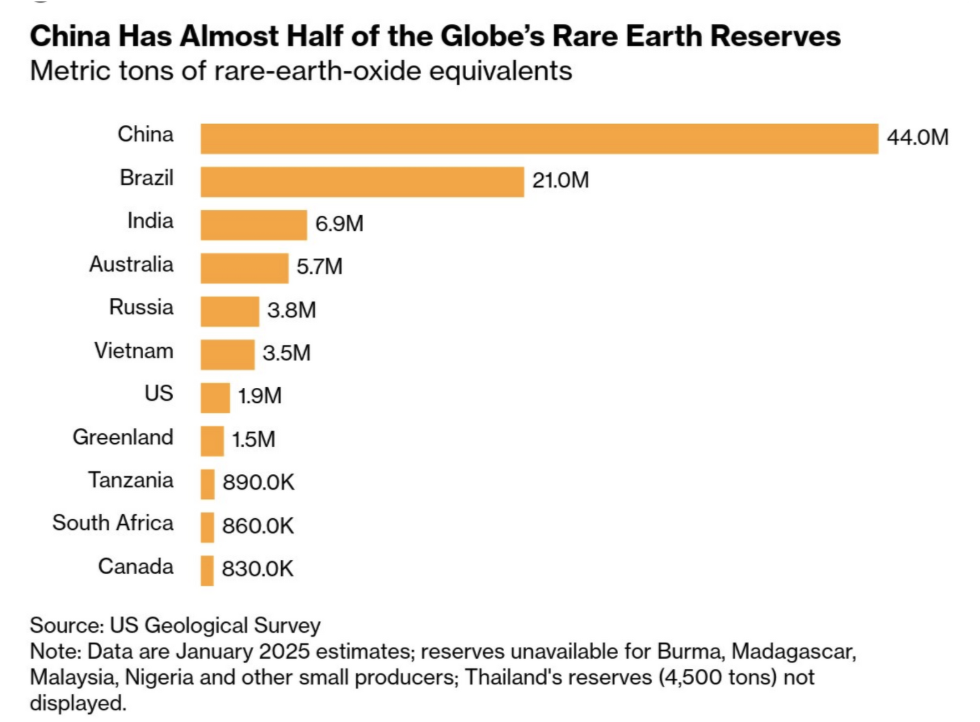

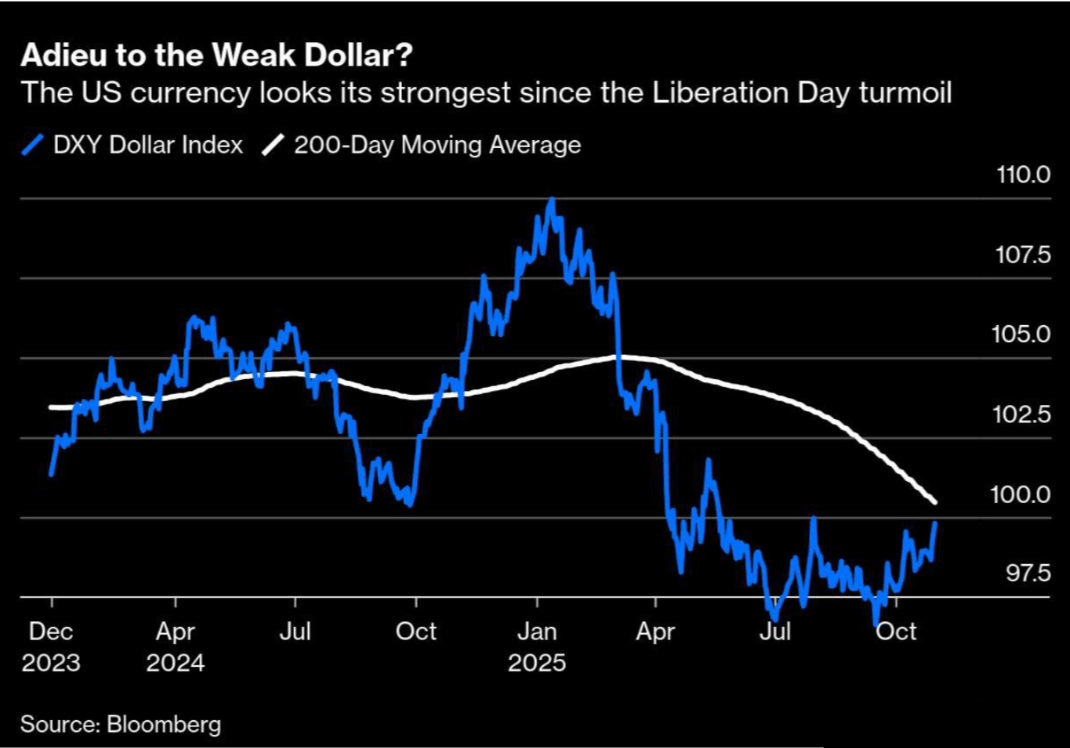

| | | | Big Tech is still pouring billions into AI, but Wall Street is making something very clear: not all AI spending is created equal. Amazon (AMZN) and Alphabet (GOOG) got rewarded, with both stocks rising on the view that their AI bets are already translating into real business, especially through cloud. Amazon in particular scored a new all-time high after highlighting progress in its infrastructure build-out and a $38 billion deal with OpenAI. On the flip side, Meta (META) is spending just as aggressively, but without a cloud platform to monetize that spend, investors aren’t convinced there’s a near-term payoff. As JPMorgan put it, the cost load is “outsized” compared to Alphabet and Amazon, which have far clearer commercialization paths. In other words, AI spending by itself isn’t a bullish story anymore. The market now wants proof, or at least a somewhat believable roadmap. “Overinvesting is in the eye of the beholder,” Schwab’s Kevin Gordon said and that’s the whole game right now. 📈 Where it goes from here Despite the mixed reaction, the AI spending wave isn’t slowing. Big Tech can self-fund most of this expansion, which is why many analysts think that even if this is a bubble, it still has room to run. But the bar is rising. As depreciation, data center build-outs, and long-term debt start to weigh on forward estimates, analysts are shifting focus to which companies can actually convert AI spending into revenue. Meanwhile, sector sentiment remains upbeat, with the Roundhill Mag 7 ETF (MAGS) ending the day higher. | | | | | The rare earth trade just lost one of its biggest accomplices: trade-war fear. Washington and Beijing moved to freeze a key front of their trade standoff. The U.S. is pausing new tariffs, and China is suspending additional export controls on rare earth materials. The White House says China will issue general export licenses again, effectively rolling back the supply curbs that fueled months of price spikes and geopolitical anxiety. Trump summed it up by declaring the “threat is gone.” USA Rare Earth dropped 13% on the day, extending a multi-week slide from its record high. 🔍 The bigger picture JPMorgan called rare earths the “unsung heroes” of the AI economy. They are used in everything from EV motors to wind turbines to data centers. So the structural demand story is still intact, even if the fear premium comes off. Oxford Economics estimates that any partial supply disruption would shave roughly 1% off U.S. growth and 0.4% off China’s over the next two years... ... which is why neither country is expected to walk away from this space. JPMorgan’s takeaway is that investors should stay diversified across the entire AI supply chain instead of piling into miners alone. Roundhill’s Critical Materials ETF fell more than 2% on the day. | | | | 💵 The dollar is reclaiming its safe-haven status | | | | The dollar is trading near a three-month high, while the yen and several other major currencies slumped as traders shifted back toward stability and liquidity. A strengthening dollar is a result of both a resilient U.S. economy and the fact that most other regions look somewhat riskier right now: -

A more cautious Fed outlook has helped keep U.S. yields higher -

The limited data available still suggests steady demand and hiring -

Inflation in Europe and rate uncertainty in Japan make the dollar comparatively more attractive So investors are rotating back into the greenback as the “just in case” trade. 🌍 The bigger picture Debt and inflation are still long-running risks for the dollar’s stability. And globally, more countries are trying to reduce reliance on the U.S. currency. The BRICS bloc continues to push for expansion, with China and Brazil backing Malaysia’s bid to join. Trump called it “an attack on the dollar” and floated new tariffs on India in response. Whether or not that happens, the effort itself highlights a growing de-dollarization trend. Meanwhile, Europe is moving ahead with a digital euro project targeting a 2029 launch, signaling growing demand for alternative payment systems. For now, the dollar holds its crown as the world’s default currency... not because everything is great, but because everything else looks worse. The U.S. Dollar Index approached 100 yesterday, up from below 96 in September. | | | | Rate today's newsletter*... | | | * We are just a messenger. To avoid confusion, please rate the quality of reporting, not news | | | | | | | | | | | | InvestorsObserver | | You received this email because you signed up on our website or made a purchase from us. | | | | |