| | Good morning, Ciena was the Nvidia of the ’90s internet boom. It was supposed to be one of the most valuable companies of that era… But when the dot-com bubble burst, the stock crashed 96% and never recovered. Here's why. Ciena was the first company to commercially deploy WDM, a technology that dramatically increased the bandwidth and cost-efficiency of fiber-optic infrastructure. Think of it as the ChatGPT moment of the internet. Under (retrospectively naive) projections that internet bandwidth would double every three months, telecoms poured over $500 billion — mostly financed with debt — into laying fiber-optic cables. The problem was that internet adoption estimates were way off. The internet changed the world, but not as fast as expected. At the end of the day, 85% to 95% of fiber laid in the ’90s remained unused after the bubble burst. AI is following a dangerously similar pattern. America’s cloud giants (aka hyperscalers) alone will spend $400 billion on AI data centers. Then there’s Stargate with $500 billion and the UAE’s $1.4 trillion pledge to invest in U.S. AI infrastructure. All that spending is driving growth estimates, which in turn are driving valuations and AI economics to absurd levels. Some AI engineers now have $100 million packages, and there's a rumor of a $1 BILLION hiring bonus. Even Sam Altman says AI is a bubble. Meanwhile, DA Davidson's Gil Luria told me top AI software companies — including OpenAI, Salesforce, and Adobe — have only generated a few tens of billions from AI. Who, how, and when will fill the gap between trillions in spending and a couple of hundred billion in revenue? Nobody knows. This week may bring more clues. Not because of earnings, but because NVIDIA, AMD, Meta, Broadcom, and Microsoft are all hosting conferences that should provide some insights into the state of AI economics. Let's dive in. P.S. To get more updates, follow IO and me on Linkedin.

| | | | | Hang tight, Dan Runkevicius, Chief Editor | |  | | | | | "We have cited for many months that healthcare has made up a very large portion of the jobs gained over the last two or three years, but with it now showing some tangible signs of decline, the foundation underneath the labor market seems to be cracking." — BlackRock’s Rick Rieder

| | | | | Five things to know before opening bell | |

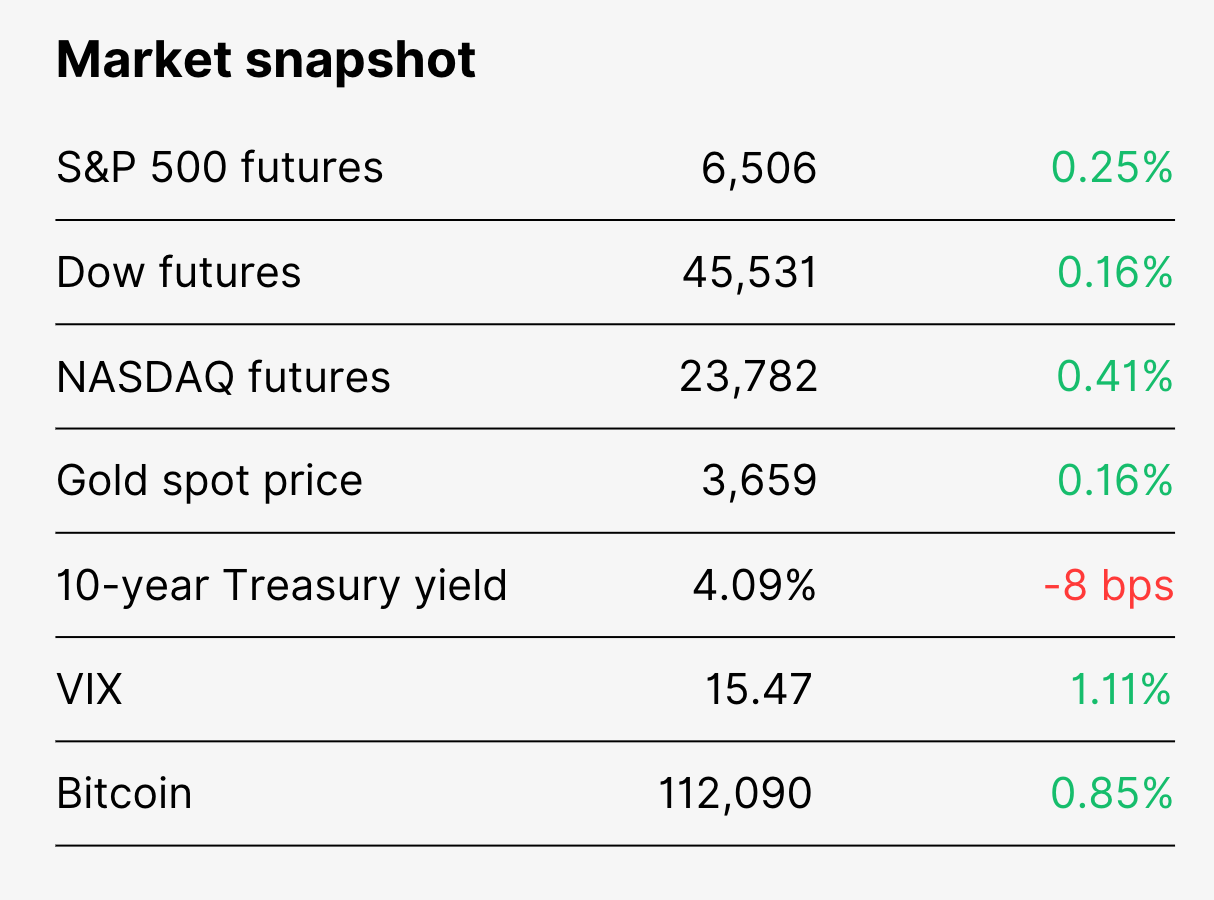

🚗 Tesla’s $1T payout sparks firestorm Tesla’s dangling a $1 trillion paycheck for Elon Musk and critics say he doesn’t have to do nearly enough to earn it. The package hinges on Tesla hitting moonshot goals over the next decade: selling 20 million cars, signing up 10 million Full Self-Driving subscribers, putting 1 million robotaxis on the road, and cranking out 1 million humanoid robots. Oh, and reaching an $8.5 trillion valuation with $400 billion in annual earnings. The board calls it a blueprint for becoming the world’s most valuable company. Skeptics call it another Musk promise factory. The vote comes in November. 🛢️ OPEC+ hints at a production cool-off Oil’s summer pump looks over. After months of ramping up supply, OPEC+ is signaling production will flatten starting next month. October’s increase is pegged at just half of September’s 547,000 bpd boost, even as sanctions on Russia and Iran keep crude above spring lows. Global demand is sputtering, and prices have drifted down for a week straight. “It’s kind of a perfect storm,” said Phil Flynn at Price Futures Group. “The OPEC story, the jobs report — it all points to a weaker market.” 🪙 Trump carves out new tariff exemptions Gold got a golden pass. So did graphite, tungsten, and uranium, under Trump’s latest executive order tweaking his import tariffs. Effective today, those metals are exempt, while aluminum hydroxide, resin, and silicone get slapped with new duties. U.S. trade partners welcomed the shift, with EU trade commissioner Maros Sefcovic saying it “paves the way” for auto tariffs to drop to 15% while securing key carve-outs. 💻 Big Tech’s big week The Nasdaq is still in the driver seat, but how long can the AI sugar high last? We may get clues in the next 72 hours as Nvidia, AMD, Meta, Broadcom, and Microsoft all take the stage at industry conferences. Apple joins the pile with tomorrow’s iPhone launch, where analysts say it needs to prove it has an AI story or risk getting left behind. 📉 Bitcoin and gold are stealing the show All three indexes closed slightly red on Friday after the weak labor print, with the Nasdaq slipping less than the Dow and S&P. Bitcoin spiked above $113,000 on the data before settling back into the $110K–$111K range over the weekend. Gold stole the show, setting a fresh all-time high above $3,600 an ounce and extending gains into Sunday. Bonds remain the market’s wild card, with traders bracing for more swings ahead of fresh data releases and the Fed’s Sept. 17 rate-cut call. | | | | 🤔 What Wall Street makes of Friday's terrible jobs report

| | | | Wall Street couldn’t stop talking about Friday’s labor market report and for good reason... 🐢 The slowdown continues The Bureau of Labor Statistics capped off a week of lackluster labor updates with an August jobs report that landed with a thud. It was the final major employment reading before next week’s FOMC meeting and it wasn’t pretty: 📊 Economists expected 75,000 new jobs (down from July’s 79,000). -

🚨 The BLS reported just 22,000 new jobs. -

📉 Unemployment ticked up to 4.3%, the highest since 2021.

🔮 What investors should expect The headlines are ugly, but analysts aren’t calling it a collapse just yet. EY chief economist Gregory Daco called the report “fairly weak,” noting employers are “being very cautious with who they hire and how much talent they want to retain on hand.” Still, he stressed the labor market “is not collapsing.” Steve Sosnick, chief strategist at Interactive Brokers, seconds Daco, saying the data “reinforces the idea of rate cuts” but “wasn’t a catastrophe” and “will be taken as a decent sign by the markets.” Not everyone is shrugging it off, though. Gary Hoover of Tulane University pointed to the 7.5% Black unemployment rate as a “telltale sign of the direction of the economy and what we can expect to see hit overall in a few months.” ⚠️ The bigger risk Markets will show their hand this week after traders digest the data, but strategists are already worried about another curveball. After President Trump blasted the BLS and fired its chief earlier this year over a weak report, some fear political distrust of economic data could add fuel to the global “sell America” trade. That, in turn, could weigh on U.S. stocks well beyond one bad jobs print. | | | | 🏛️ Is it too late for inflation to sway the Fed? | | | | Friday’s jobs flop has made it clear: the labor market is now a bigger headache than inflation. But the Fed can’t ignore prices, especially with fresh CPI data hitting just days before policymakers meet. 💯 Investors are betting on cuts A 25bp cut on Sep as a lock. Odds were already above 90% before Friday’s shocker, and the BLS’s dismal 22,000 jobs print sealed it. Even Bank of America, long one of the more hawkish holdouts, has thrown in the towel. “The August jobs report should cement a shift in the Fed’s thinking from worrying about inflation to focusing on labor weakness,” BofA Global Research said in a note. The bank now expects two 25bp cuts this year, followed by another 75bp in reductions through 2025, with the door open to “possibly more” in 2026. 🏛️ Fed not fully convinced The consensus on Wall Street doesn’t mean unanimity inside the Fed. July’s FOMC meeting already showed rare dissent, and Chicago Fed president Austan Goolsbee said he’s still undecided heading into this month’s vote. That’s where Thursday’s CPI report comes in. Economists are calling for a 2.9% annual and 0.3% monthly rise. But as Sarah House and Nicole Cervi wrote, the July CPI “indicated that tariffs are not the only challenge” holding back disinflation. Sticky services costs and rebounding goods prices are pushing inflation further from the Fed’s 2% target and could give hawks ammunition to argue against cutting too aggressively. 🃏 The 50bp wildcard The smart money remains on a 25bp trim next week. But after such a glaring jobs miss, weekend chatter turned to whether the Fed might surprise with a 50bp cut. Leslie Falconio at UBS Global Wealth Management isn’t buying it, though. "We all know that September, the 25 basis points was a done deal. I don’t think this is weak enough to push it to the 50, but I do think the market was already really ahead in terms of pricing in this weakness within the labor market.” | | | | 📬 Mail traffic plunges after 'de minimis' cutoff | | | | While most headlines zero in on Trump’s tariffs against trading partners, one of his most consequential trade moves has flown under the radar... It's shutting down the long-standing “de minimis” exemption. The rule once let sub-$800 imports bypass U.S. duties. Now that it’s gone, foreign sellers have lost their edge and the fallout is showing up in America’s mail trucks. 🚚 Emptier mail trucks everywhere The Universal Postal Union (UPU) reports a steep, abrupt plunge in U.S.-bound mail since the rule change. According to its data: “The global network saw postal traffic to the U.S. come to a near-halt after the implementation of the new rules on Aug. 29, 2025,” the Switzerland-based group said, noting that customs duty collection is now pushed onto carriers or CBP-approved intermediaries. 📜 A little historical perspective The de minimis carve-out isn’t new. It first appeared in 1938, exempting imports worth $1 or less. Congress later raised the bar: -

1990: raised to $5 -

1993: bumped to $200 -

2015: lifted to $800 Cheap cross-border e-commerce supercharged its use. By last year, 1.36 billion packages worth $64.6B entered under the exemption, more than 10x the 134 million that came in a decade earlier. ⚖️ Where things stand now Exporters and postal operators say the U.S. gave too little warning and guidance, leaving them scrambling. But the White House defends the move as closing a loophole long abused by counterfeiters and drug smugglers. There are only a few carve-outs left: gifts under $100 and personal souvenirs under $200. For everyone else, the era of duty-free imports under de minimis is over. | | | | Rate this newsletter | | | Your feedback matters! Before you go, please rate this newsletter and share your thoughts. | | | | | | | | | | | | InvestorsObserver | | You received this email because you signed up on our website or made a purchase from us. | | | | |