| | Good morning, Small caps stole the show yesterday, with the Russell 2000 ripping to an all-time intraday high and leaving the megacaps in the dust. Intel also shocked Wall Street with a 23% surge after Nvidia poured $5 billion into the struggling chipmaker, marking its best day in years. Meanwhile, Wall Street is still trying to game out whether Powell just made a one-off move or opened the door to a full cutting cycle. Muddying the picture, jobless claims came in better than expected, throwing cold water on the “weak labor market” narrative that supposedly justified the cut in the first place. Elsewhere, gold and silver flipped lower, the dollar bounced, Bitcoin ticked higher, and IPO fever looks alive again with Netskope’s hot debut. Even restaurant chains made the headlines. Cracker Barrel blamed a logo fiasco for its slump while Darden warned it’s not just signage: consumers are pulling back on eating out. Plenty of moving parts, plenty of contradictions. Let’s dive in.

| | | | | Hang tight, Dan Runkevicius, Chief Editor | |  | | | | | “I think it’s much more prudent for the Fed to be looking at all the models, to have a diversity of opinions and decide, ‘What are we going to do in this economy that really looks to be taken off with inflation that’s decelerating, but higher than the target?’ They split the baby in this decision, and I think that’s probably a pretty prudent call.” — National Economic Council Director Kevin Hassett | | | | | Five things to know before opening bell | |

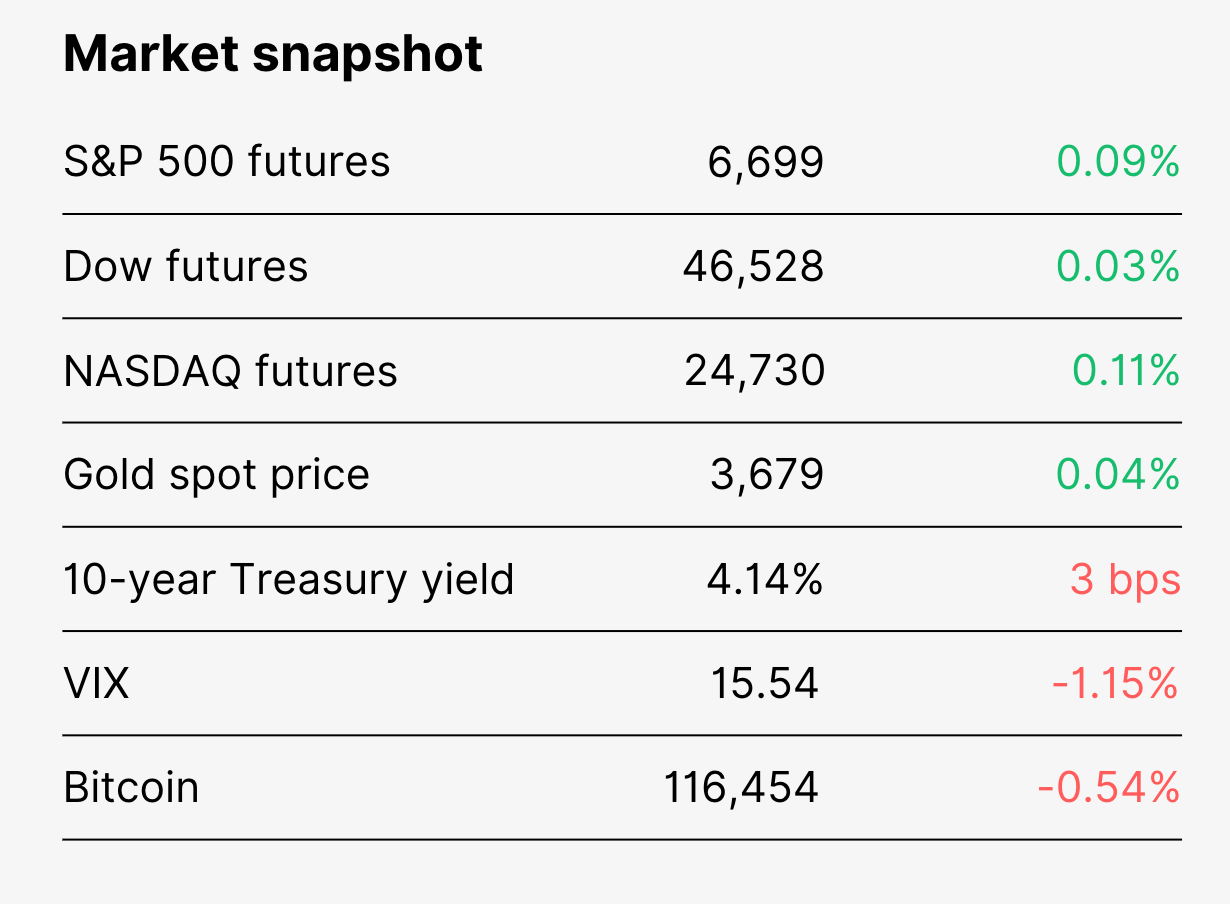

📈 Small caps lead Thursday’s surge Rate-cut euphoria lit up markets again yesterday, but this time it wasn’t Big Tech carrying the torch. The Russell 2000 jumped more than 2% to a fresh intraday high, while the Nasdaq added 0.94%. Smaller, more speculative names tend to pop hardest after cuts since they rely more on outside funding and Morgan Stanley says this could kick off “a more durable rotation to small caps and lower quality stocks.” 🏭 Philly Fed shows manufacturing pickup The Philly Fed’s September survey surprised to the upside, posting its strongest reading since January at 23.2 (vs. 15.9 in August). Gains showed up in activity, new orders, and shipments, while employment stayed flat. But not everything was rosy. Capex forecasts dipped, inflation fears remain high, and executives warned the sector is still volatile. But for a manufacturing outlook that’s been gloomy most of the year, this was welcome news. 💰 Metals and dollar flip after Fed cut Gold and silver were climbing toward records before the Fed’s 25bp cut, but both reversed on Thursday as the dollar bounced back. The US Dollar Index, which briefly hit a 2025 low after the announcement, closed about half a point higher at 97.5. Gold futures slid more than 1% before settling around $3,680 an ounce. 🚀 IPO window swings wide open Cybersecurity player Netskope popped 18% in its Nasdaq debut, with CEO Sanjay Beri pointing to AI and cloud demand as long-term tailwinds. Analysts say the timing couldn’t be better. The Fed cut has cleared a key hurdle, and bankers expect a packed October IPO calendar. “There were certainly companies waiting to get through this… expect a very full calendar,” said Truist’s West Riggs. 🤝 Intel-Nvidia pact fuels AI optimism Intel shares exploded 23% after Nvidia announced a $5 billion investment, its biggest single-day pop in years. The tie-up will fund joint production for PCs and data centers, and it adds to Intel’s recent $9 billion lifeline from Washington and $2 billion from SoftBank. Nvidia also climbed nearly 3.5% on the news. | | | | 💼 Labor numbers look good… sort of

| | | | The Fed just cut rates to ease rising unemployment... but 24 hours later, fresh jobs data made that call look a little premature. New jobless claims fell hard last week, dropping 33,000 to 231,000, which is well below the 241,000 economists had penciled in. Continuing claims also slipped to 1.92 million, with the four-week average edging down to 240,000. 🔄 Big reversal from last week That’s a big reversal from the prior week, when filings spiked to their highest since Covid and gave cover for the Fed’s move. Markets read yesterday’s report as a sign the labor market isn’t quite rolling over. After the release, bond yields and gold steadied, keeping volatility in check. Add in August’s stronger-than-expected consumer spending, and analysts say retail stocks tied to employment trends could see a short-term lift. But for the Fed, the whiplash in the numbers only makes the next move harder to call. | | | | 🥴 Cracker Barrel earnings take a hit... but is it all about the logo? | | | | Weeks after criticism of its new logo and store redesigns sparked a sell-off, Cracker Barrel delivered an underwhelming earnings report... and the backlash probably didn’t help. 📉 How they got here Almost a month after rolling out its ill-fated new logo, Cracker Barrel’s stock fell 7.64% on Thursday following the earnings report. Shares had clawed back some ground but are still down nearly 17% for the year. Earnings highlights: -

Traffic has dropped roughly 8% since the August 19 logo rollout -

Current-quarter traffic is expected to stay down about the same -

Adjusted EPS came in at $0.74, six cents below expectations -

Revenue fell 3% for the quarter, slightly better than analyst projections CEO Julie Masino addressed the backlash ahead of the report, pledging to “switch back to our ‘Old Timer’ logo, hitting pause on remodels, and placing an even bigger emphasis in the kitchen and other areas that enhance the guest experience.” 💸 A symptom of a bigger issue Cracker Barrel is not alone. Darden Restaurants, which owns Olive Garden and other national chains, also reported weaker-than-expected profits.

Experts say fast-casual chains across the country are feeling the pinch of a cooling economy as budget-conscious consumers are cutting back. “Tightening the belt on restaurant spending is one of the earliest signs that households are feeling economic strain. It’s not just about skipping a night out — it’s about families making daily trade-offs,” said George Washington University professor Todd Belt. | | | | 🤷 Where are rates headed next? | | | | Wall Street celebrated Wednesday’s cut, but now everyone is trying to figure out if it was a one-off or the start of a full cutting cycle. Strategists are making guesses, but the signals are all over the place... 🗣 Powell’s cautious take After months of a wait-and-see approach, Fed chair Jerome Powell stayed tight-lipped post-cut. “We’re in a meeting-by-meeting situation. Actual decisions we make are going to be based on the incoming data, the evolving outlook, and the balance of risks at the time the decisions are actually made,” he said. He called the economy “such an unusual situation,” with both sides of the Fed’s dual mandate — inflation and labor — trending the wrong way. “So we have a situation where we have two-sided risk,” Powell said. “And that means there’s no risk-free path; and so it’s quite a difficult situation for policymakers.” 🦅 Hawks vs. 🕊 Doves Analysts are split. Goldman Sachs chief US economist David Mericle expects more cuts. “We continue to expect 25bp cuts in October and December — with a 50bp cut possible if the labor market weakens more than we expect,” she wrote in a note to clients. Mericle sees additional cuts next year bringing rates to 3.00%-3.25% and notes that “risk-management” cuts like Wednesday’s are almost always followed by more. On the other hand, Appaloosa Management president David Tepper warned against overplaying it. “If they go too much more on interest rates, depending what happens with the economy … it gets into the danger territory. You’ve got to be careful not to make things too hot,” he said. The CME FedWatch tool, which priced in a 96% chance of Wednesday’s cut, now shows an 88% probability of another cut next month and a 75% chance of one in December. So while most expect more cuts, the path forward is anything but clear. | | | | GIFs in newsletter: Yes or no? | | | Your feedback matters! Before you go, please cast your vote! | | | | | | | | | | | | InvestorsObserver | | You received this email because you signed up on our website or made a purchase from us. | | | | |