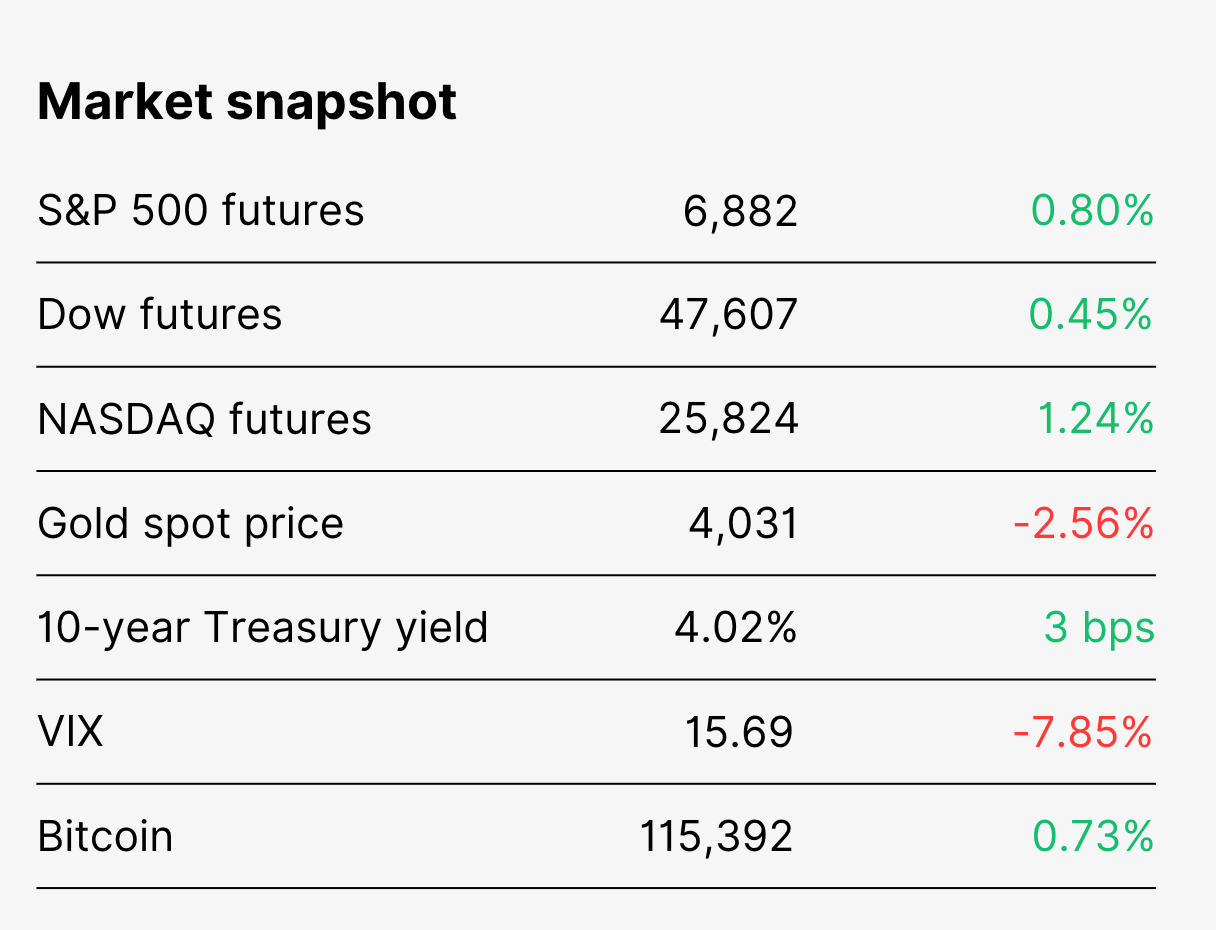

| | Good morning, Instead of the usual rundown of what to watch today, I’ve got a small favor to ask. Over the past few months, a lot of you have sent emails with tips on how to make the Morning Brief an even better pre-market read. First off, thank you for taking the time; I’ve read every single message. Some ideas I’ve already quietly rolled out, others are parked for later. Speaking of which, the majority of requests (probably nine out of ten) boils down to more data. So far, we’ve tracked the key benchmarks: stock futures, gold, the 10-year yield, the VIX, and Bitcoin, which cover most portfolios and general mood. But since there have been so many requests to expand that daily widget, I can't help myself. Before we make any changes, spare a few moments in the survey below. If you have more ideas, be sure to vote and leave them in the open question box that follows. Have a lovely Monday! | | | | | Hang tight, Dan Runkevicius, Chief Editor | |  | | | | | “If what people are worried about is we’re going to get some trade deal where we’re going to get favorable treatment on trade in exchange for walking away from Taiwan — no one is contemplating that.” — Secretary of State Marco Rubio, on US-China trade talks | | | | | Five things to know before opening bell | | |

🇺🇸🇨🇳 Trade truce coming? Looks like Trump and Xi might finally be ready to shake hands... or at least stop throwing punches. Top negotiators from both sides wrapped two days of talks in Malaysia saying they’d reached “broad consensus” on a slew of thorny issues, from export controls to fentanyl to shipping levies. 😬 Americans don't buy CPI numbers Inflation may be cooling on paper, but Main Street isn’t buying it. The University of Michigan’s sentiment index just hit its lowest level since 2022, with nearly half of Americans saying rising prices are eating into their finances... and even more bracing for higher unemployment next year. 💼 Earnings avalanche this week Big Tech dominates earnings this week, with Microsoft, Amazon, Apple, Alphabet, and Meta all reporting. Their results could decide whether the AI-driven rally still has fuel or finally needs a breather. Energy giants Exxon Mobil, Chevron, Shell, and TotalEnergies are also on deck, plus UnitedHealth and Verizon from the defensive crowd. Expect volatility... and plenty of it. ⚡ Bitcoin Miners get an AI makeover Faced with thin margins and wild token swings, they’re pivoting hard into AI. IREN, Riot, TeraWulf, and Cipher Mining are repurposing their data centers into high-performance compute hubs built for AI workloads. Cheap energy access gives miners a serious edge in the AI arms race. Turns out the rigs that once minted tokens might soon be powering the next GPT. 🍁 Trump vs. Canada: Round two Trump’s throwing fresh tariffs north of the border again. The president slapped a new 10% duty on Canadian imports this weekend, accusing Ontario officials of “fraudulently” editing a Ronald Reagan clip to mock his trade policies. The move effectively freezes talks between Washington and Ottawa, just weeks before the Supreme Court weighs in on Trump’s tariff powers. Ontario Premier Doug Ford said the ad will pause today, “but not before reaching U.S. audiences at the highest levels.” | | | | 🎭 The good, the bad, and the shrug of CPI

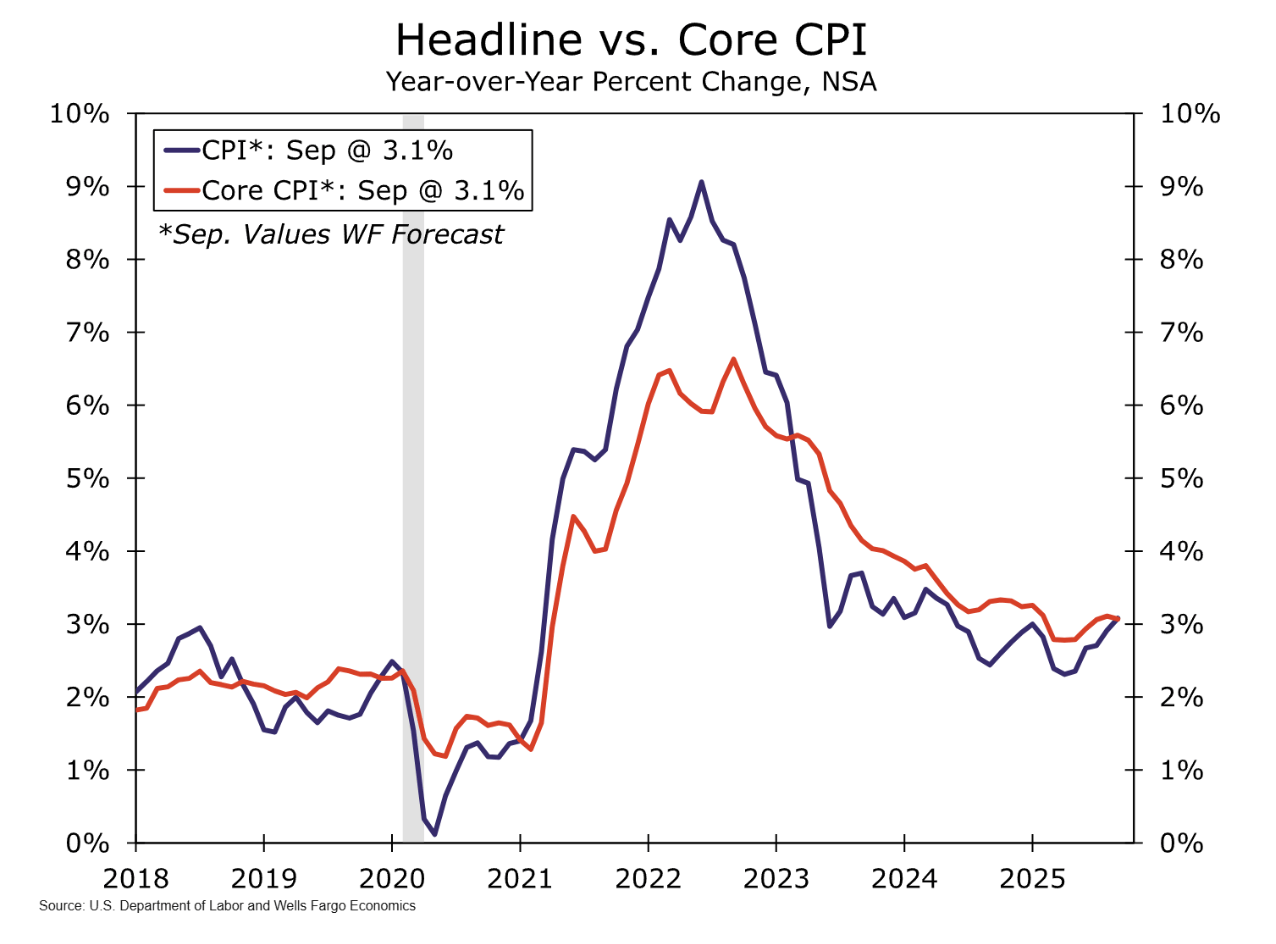

| | | | After weeks of radio silence, the Bureau of Labor Statistics finally broke the shutdown-induced blackout on Friday, releasing the Consumer Price Index. The agency called staff back to work just to get this one out, since CPI determines cost-of-living adjustments for Social Security recipients. But for investors, it’s more than a bureaucratic formality. It’s the first official read on inflation before this week’s Fed meeting. 📊 By the numbers Headline inflation ticked up 0.1 percentage point, while core CPI (which strips out food and energy) ticked down 0.1, leaving both at an even 3.0% annual rate. That’s still above the Fed’s 2% target, but a hair below the 3.1% economists expected. -

🛢️ Gasoline jumped 4.1% month-over-month, the biggest driver of September’s inflation -

🏠 Shelter rose just 0.2%, its smallest monthly gain since 2021, now up 3.6% year-over-year -

👕 Apparel prices climbed 0.7%, which analysts largely blamed on tariffs -

📈 Overall: headline CPI rose 0.3%, core rose 0.2% In other words, inflation is not dead, but it’s not out of control either. 🧠 What analysts are saying TradeStation’s David Russell had one of the more upbeat reads. “Inflation might not be slowing, but it’s not surprising to the upside anymore. The details are positive, with shelter and transportation services moderating," he said. "Some key parts of the basket are cooling even if tariffs nudge budget items like apparel higher.” Marked are largely on board with this view, all three major indexes closed at record highs Friday, capping the week with a collective sigh of relief. But not everyone’s popping champagne. ING’s chief international economist James Knightley cautioned that the numbers don’t mark a real turning point. “The ‘realized’ tariff rate has only been around 10% so far due to mitigation measures that won’t last forever.” Knightley pointed to a “strong substitution effect” as companies reroute supply chains through lower-tariff countries to dodge costs. “In time we expect the realized tariff rate to rise and goods prices to be more heavily impacted,” he added. “But we continue to argue that tariffs will be a one-off step change in prices rather than something that will lead to more persistent inflation.” 🏦 Why it matters With rate-cut expectations still alive going into the Fed’s midweek meeting, this report lands right in the middle of the hawk-dove crossfire. Inflation is not high enough to kill rate cut plans but not low enough for Powell to declare victory either. Wall Street is happy, Powell not su much... | | | | 🏦 Everyone knows what will happen on Wednesday, but then what? | | | | The Fed is about to make a move everyone already sees coming, but what happens after could be the real test. The long-delayed CPI report finally gave Powell another excuse to cut rates on Wednesday, but the shutdown has frozen most of the government’s data flow, including jobs reports. As Goldman Sachs’ Lindsay Rosney said, the Fed is essentially “flying blind,” which is never a great way to steer a $28 trillion economy. Even Fed Chair Jerome Powell has admitted the blackout is making his job exponentially harder. And JPMorgan’s Michael Feroli warns that time’s running out. “I would say after Thanksgiving you probably want to have that,” Feroli said of the pivotal market indicators. “Fed officials kind of have a sense of the message that they want to give to the market about December. And so if you go past November, I think then they’re going to have some issues in terms of how they’re talking about policy to the market.” Translation: if the lights don’t come back on soon, the Fed’s next meeting could be pure guesswork. 🏜️ What's next? After Friday’s inflation data, the CME FedWatch tool now shows a 98% probability of a rate cut on Wednesday and few are arguing. Looking ahead to December, futures traders are pricing in one more cut before the outlook disappears into the fog. Between domestic gridlock and international trade flare-ups, the economy in constant flux, and without real data, the Fed’s dashboard is blinking red. For now, policymakers, CEOs, and investors are all in the same boat: they’re guessing, adapting, and hoping the next data drop comes before the next crisis. | | | | | We’ve talked before about America’s “K-shaped” recovery in household income. That divide’s no longer just about earnings. Ot’s now splitting the market itself. A handful of AI-linked industries are booming, while much of the economy is hardly budging under tariffs, rising costs, and weakening demand. 🤖 AI boosts its friends (for now) It’s no secret that AI has been the biggest driver of this bull market. Money’s been flooding into anything with a whiff of AI exposure, sending valuations to absurd heights. Just look at the energy sector: - ⚡ Power providers have seen their median price-to-sales ratio triple since 2023

☢️ Nuclear startups Oklo and NuScale Power trade at multibillion-dollar market caps despite minimal revenue and zero near-term profits - 🏗️ AI-powered data center developer Fermi launched at a $19 billion valuation before even breaking ground

Big Tech’s nuclear gold rush is spilling over too, with traditional names like Constellation Energy posting their strongest yearly gains on record. While it’s been a lucrative ride for early believers, it’s left the market with an AI-centric reward system that glorifies moonshots and leaves legacy industries out in the cold. 🧮 Where hype meets reality Last month, JPMorgan estimated that 1.1% of all U.S. GDP growth now comes directly from AI capex, officially surpassing consumer spending as “an engine of expansion.” That’s a staggering figure — but even if AI spending props up growth through the slump, it’s not an instant fix. As Hatim Rahman of Northwestern’s Kellogg School of Management warned, AI is not a “plug-and-play solution” that will miraculously boost productivity. “It’s going to involve engagement with people, processes, culture, tools to be able to reap the benefits. And in the aggregate, it’s going to take some time,” he said. Meanwhile, capex investments are climbing by the trillions and widening the breakeven gap. 🏚️ Meanwhile, in the real economy… Outside the AI bubble, the picture’s a lot rougher. Small businesses are under pressure, consumer sectors are soft, manufacturing’s been shrinking for seven straight months, and construction’s flatlined. Layoffs are creeping back too, including Target’s announcement Thursday that it’ll cut about 1,800 corporate jobs. “I think the message that the AI economy is sort of driving up the GDP numbers is a correct one. There may be weakness in the rest of the economy, or not weakness, but there may be more modest growth,” said NYU’s Arun Sundararajan. Recent sentiment data confirms that Main Street isn’t feeling as flush with cash as Wall Street. | | | | What data should we add to our daily dashboard? | | | | | | | | | | | | | | | InvestorsObserver | | You received this email because you signed up on our website or made a purchase from us. | | | | |