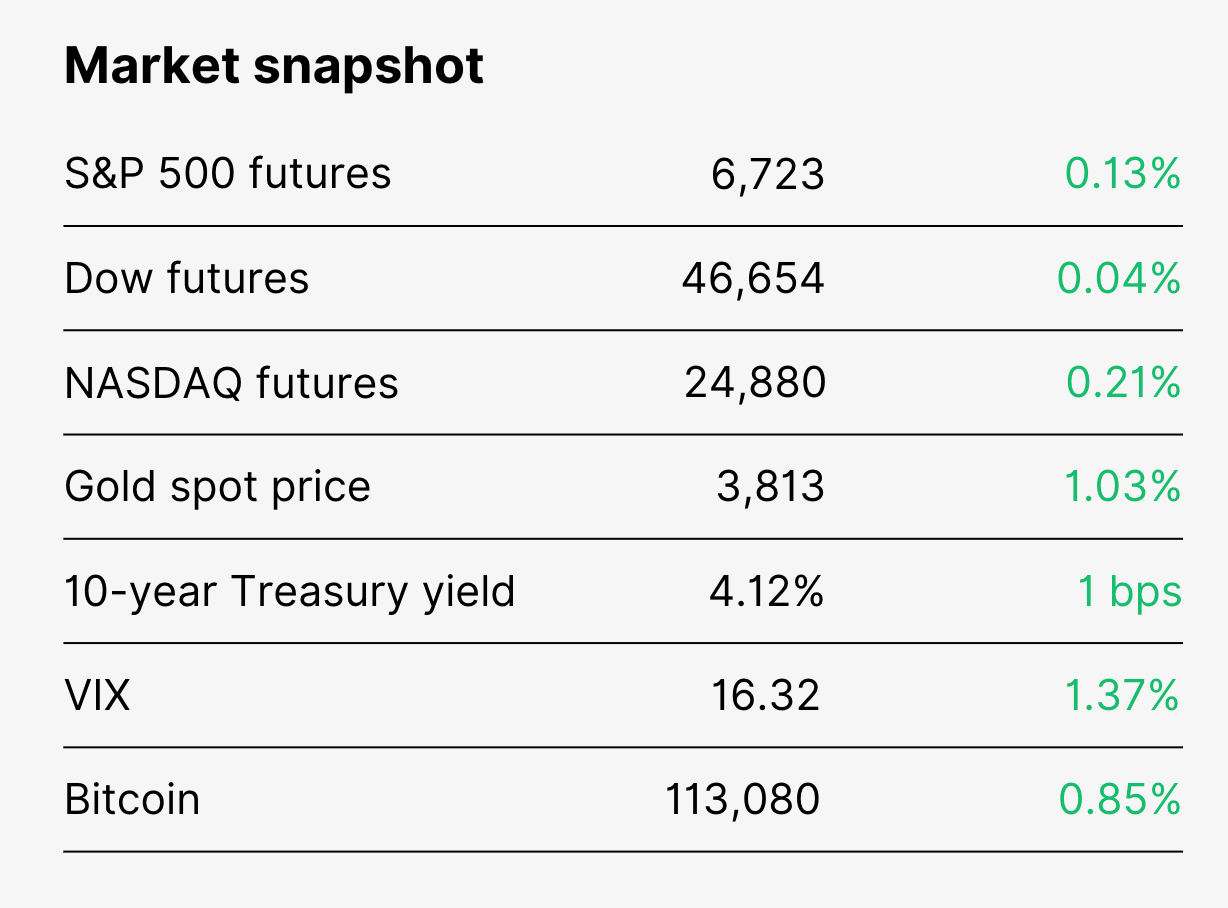

| | Good morning, Stocks faltered yesterday, but Wall Street is clinging to the idea that AI, productivity gains, and a friendly Fed could keep the rally alive. Meanwhile, gold hit $3,800 an ounce, with analysts now talking $4,000 in the face of geopolitical tension, inflation worries, and rate-cut hopes. Crypto ETFs have also tagged along this time, with nearly $2 billion in inflows last week, though Bitcoin itself remains stuck just under $112,000. On the economic front, the Chicago Fed debuted its new twice-monthly real-time unemployment gauge, pegging September at 4.3%, while PMI data and a record drop in imports hint at a slowdown in domestic growth. While Wall Street banks on the Fed as a backstop, Powell reminded yesterday that lower rates can be a double-edged sword in today’s setup “Two-sided risks mean that there is no risk-free path,” he said, signaling the Fed is walking a tightrope between slowing employment and stubborn inflation.

It’s a week of data, decisions, and debates and the markets are watching every move. Let’s dig in. | | | | | Hang tight, Dan Runkevicius, Chief Editor | |  | | | | | "Although tariffs were again cited as a driver of higher input costs across both manufacturing and services, the number of companies able to hike selling prices to pass these costs on to customers has fallen, hinting at squeezed margins but boding well for inflation to moderate." - S&P Global executive director Chris Williamson | | | | | Five things to know before opening bell | | |

🆕 New unemployment gauge

Meet the Chicago Fed’s new twice-monthly “real-time” reading. Pulling data from ADP, Indeed, Google, and the government, the first forecast pins September at 4.3%. “One of the hardest things a central banker has to do is get the timing right in moments of transition, and that’s why real-time data can be so important,” said Chicago Fed president Austan Goolsbee. 📉 US imports hit rock bottom in Q2 The latest Bureau of Economic Analysis data show the US current account deficit plummeted nearly 43% to $251.3 billion, the biggest quarter-over-quarter drop on record. Analysts expected a decline, but not that steep. Q1 had set an all-time high as companies stockpiled to dodge tariffs, making Q2’s plunge more pronounced. ⚠️ Powell warns of a “challenging situation” A week after the first rate cut, Powell flagged the narrow tightrope the Fed is walking. While rate cuts accommodate slowing payrolls, inflation hasn’t eased. Stocks slid after his speech. “Near-term risks to inflation are tilted to the upside and risks to employment to the downside,” Powell said. “Two-sided risks mean there is no risk-free path. 💰 $4K gold could be within reach Gold surged past $3,800 yesterday as investors seek safety in the face of war, inflation, and rate-cut speculation. Analysts are raising targets fast. Goldman Sachs now expects $4,000 by mid-2026, with the potential for $4,500 or even $5,000 if demand holds. 🚀 Rate cut fuels crypto inflows Last week’s 25bp trim barely moved stocks at first, but crypto ETFs felt the impact soon after. CoinShares reports $746 million flowed in on Thursday and Friday alone, bringing total inflows to $1.9 billion, roughly half in Bitcoin. That hasn’t lifted BTC yet, with prices just under $112,000 as of late yesterday. | | | | 📉 PMI hints at slower US growth

| | | | S&P Global’s latest PMI signals slowing domestic business activity across the board. 📊 Key takeaways: -

PMI Composite fell a full point from 54.6 to 53.6 -

Manufacturing slipped from 53 to 52; services fell from 54.5 to 53.9 -

Signals Q3 GDP growth of roughly 2.2% year-over-year While solid by historical standards, Chris Williamson of S&P Global noted that momentum has been rolling downhill since peaking two months ago. 🌐 The OECD dials up GDP forecast Meanwhile, the OECD is banking on strong AI investments as a driver of its slightly higher 2025 GDP forecast (now 1.8%, up from 1.6%).

But slower overall expansion, higher tariffs, and falling net immigration temper the optimism. Looking ahead, the organization expects the 2026 GDP to cool to 1.5%. Meanwhile, tariffs are hitting hard. The OECD notes that after Trump’s latest duties, the US effective tariff rate hit 19.5%, the highest in over 90 years. That’s not great for US GDP, but it did push the global growth forecast up. The OECD now expects year-end global GDP of 3.2%, up from 2.9%, with 2026 set to outpace the U.S. again at 2.9%. 📌 Bottom line: US growth is slowing, global growth is holding stronger, and high-tech investment like AI remains one of the few engines still revving. | | | | ⚖️ The most divided Fed in three decades | | | | Last week’s 25bp cut made clear that unemployment is the Fed’s biggest worry, but Powell’s remarks yesterday showed just how delicate a balancing act the central bank is playing… ✂️ Fed splits are widening For the first time in three decades, July’s FOMC meeting had two dissenting votes. That was followed by another unanimous vote last week. New Fed governor Stephen Miran pushed for a jumbo half-point cut. Regional presidents in Cleveland, Atlanta, and St. Louis warned against rushing more cuts, citing inflation still a full point above the 2% target. Atlanta Fed president Raphael Bostic said another cut shouldn’t happen unless the data improves. Miran pushed back, arguing tariff-driven inflation is overblown. “With respect to tariffs, relatively small changes in some goods prices have led to what I view as unreasonable levels of concern,” he said. 🔮 Rate expectations

CME FedWatch shows just under 90% odds of an October cut, but FOMC members are split: -

Seven see no more cuts in 2025 -

Eleven expect at least one more 25bp cut -

Miran favors 1.25 points total “The chasm between the maximum and minimum dots was immense, particularly considering there are only two meetings remaining this year,” Deutsche Bank said.

All eyes are on upcoming remarks from San Francisco Fed president Mary Daly and Friday’s PCE inflation report. As Silvercrest senior analyst Marcus Viscichini explained, the Fed favors PCE over CPI for its “clearer view of actual cost-of-living changes and consumer behavior trends.” Economists surveyed by Dow Jones and WSJ expect slight increases — 2.6% to 2.7% overall and steady 2.9% core inflation — marking a fourth straight month of gains.

| | | | 📈 Wall Street optimism refuses to die | | | | The post-Liberation Day rally has already defied expectations, but keeping it going would require a few things to line up just right... strong margins, more Fed cuts, and deregulation. 🐂 What bulls say TKer analyst Sam Ro is bullish, pointing to the resilience of corporations through pandemics, inflation, and tariffs as a signal that margins could stay strong. Bank of America’s Savita Subramanian is on the same page, banking on “operating leverage, continued efficiency gains (AI and others), [and] slowing employment inflation in many labor-intensive sectors.” That’s, he says, on top of potential cost-cutting driven by Trump’s deregulation agenda. 🐻 What bears say Powell, who happens to be in the bears’ camp this time, took aim at valuations, saying yesterday that stocks are "fairly highly valued." Meanwhile, DataTrek cofounder Nicholas Colas has a more straightforward explanation: the growth trajectory is simply too steep to maintain. By his estimates, the S&P 500 would need to rise 13.4% in 2026 and another 15% in 2027 just to stay on pace with its long-term growth. ‘Investor confidence must remain well above average over the next two years for the S&P to match its long-run rate of return,’ Colas said.” 📌 Bottom line: The momentum is still there, but with so many moving parts — tariffs, labor trends, AI growth curves — assuming it will last through the year (or beyond) is a risky bet.

| | | | Rate today's newsletter... | | | Your feedback matters! Take a sec and tell us how we did! | | | | | | | | | | | | InvestorsObserver | | You received this email because you signed up on our website or made a purchase from us. | | | | |