| | Good morning, AI might be padding Wall Street’s year-end bonuses, but it’s also lighting up Texas. As oil drilling cools, a surge of data centers is rewiring the state’s shale heartland, giving producers like Diamondback Energy (FANG) a second act as electricity suppliers. Over in Europe, companies like BMW (BMWKY) and Adidas (ADDYY) are quietly winning the tariff war, posting gains that put U.S. multinationals to shame. Back home, another wave of so-called “zombie companies” is taking shape. Nearly a hundred firms fell into that category in October alone (mostly biotech) as higher-for-longer rates squeeze profits and refinancing windows slam shut. Meanwhile, small caps are flirting with record highs, bonds are breathing again, and Big Tech’s still leaning on ads to fund its AI binge. But with 92% of GDP growth now tied to that same AI boom, investors are wondering what happens when the lights flicker. Let’s get into it.

| | | | | Hang tight, Dan Runkevicius, Chief Editor | |  | | | | | "High-income households are at yearly lows for spending-cut intentions while middle- and low-income households show persistent economic anxiety." — TD Securities head of thematic content Tristan Margot | | | | | Five things to know before opening bell | | |

⚙️ Can AI save Texas shale? Texas oil drillers may have found an unlikely lifeline in AI. The Electric Reliability Council of Texas expects electricity demand to jump 40% by 2030, nearly a quarter of it from AI infrastructure. That surge is turning producers like Diamondback Energy (FANG) into surprise winners. “The result for upstream players is a profitable power business,” said Welligence’s Markus Mowatt-Larssen. 🇪🇺 Europe shrugs off tariffs European firms are weathering tariffs better than just about anyone expected. A Goldman basket tracking the continent’s most exposed exporters, including BMW (BMWKY) and Adidas (ADDYY), has rallied 6% this earnings season, doubling the Stoxx 600’s gains and tripling those of more domestically focused peers. “The impact of tariffs has so far been somewhat negligible for European companies, except in rare cases,” said Optigestion fund manager Nicolas Domont. 🎙️ Armstrong’s ‘mention market’ mic drop Coinbase (COIN) CEO Brian Armstrong ended his latest earnings call with a showman’s touch, dropping buzzwords like “Bitcoin,” “Ethereum,” and “Web3” in rapid fire to trigger prediction-market payouts on Kashi and Polymarket. Critics like Arca’s Jeff Dorman called it “open market manipulation,” but others saw it as a clever nod to the rise of “mention markets,” where traders bet on what executives will say.

💵 Bonds move from defense to offense Treasuries are showing signs of life after the 10-year yield has slipped nearly half a percentage point in 2025. BondBloxx’s Tony Kelly sees “more opportunity in fixed income” now that rates have room to fall, singling out emerging-market debt and private-credit ETFs as bright spots. 📈 Longer-dated bonds may be better positioned this cycle JPMorgan’s Jordan Jackson expects the Fed’s rate cuts to hit the short end hardest. “Three-month to two-year maturities will decline most sharply over the next twelve months,” he said. Meanwhile, a mix of big deficits, sticky inflation, and resilient growth means the 10-year yield is likely to stay anchored above 4%, with risks “skewed toward higher yields,” he added.

| | | | 🤖 Big Tech’s AI balancing act

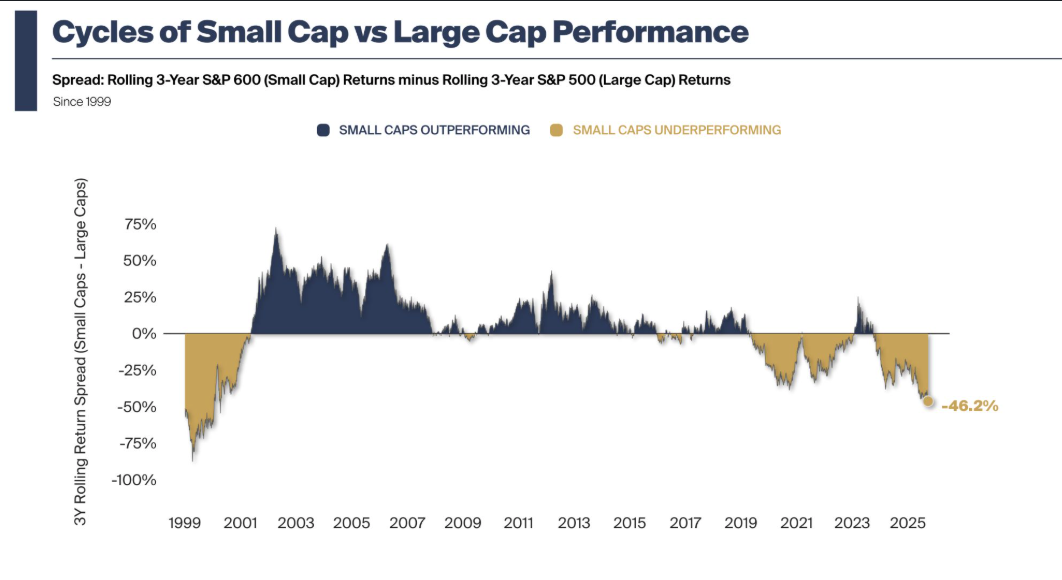

| | | | With Nvidia now worth over $5 trillion and the Magnificent Seven making up nearly one-third of the entire market, this AI rally is starting to look like a very expensive trust fall. The good news is these companies still have a cash cow to fall back on: ads. 💰 Ads keep the lights on For now, tech’s biggest names are leaning on what’s always worked: advertising. Meta, Amazon, Alphabet, and Microsoft all reported strong ad growth last quarter, with Meta and Amazon posting roughly 25% annual gains, while Reddit’s ad sales jumped 68%. That’s strong proof Big Tech can still milk its cash cows even as it pours billions more into AI infrastructure. It’s essentially the Amazon story all over again. The company funded its unprofitable e-commerce arm for more than a decade with cloud profits from AWS. AI is just a whole ’nother scale, though. According to Harvard economist Jason Furman, AI-related investment accounted for 92% of U.S. GDP growth in early 2025. The catch is, if consumer spending stalls, that ad lifeline might not hold long enough for those AI bets to start paying off. And with companies expected to sink another $400 billion into AI infrastructure this year alone, that kind of concentration risk is getting impossible to ignore. ⚡ The energy wild card AI’s invisible backbone, and its biggest bottleneck, is energy. Data centers already consume about 4% of all U.S. electricity, nearly doubling the average electricity bill compared to five years ago. Energy analysts say AI demand could easily double within the next few years. Solar and nuclear remain the most promising fixes, but both face a number of roadblocks, from red tape to supply chain bottlenecks. So the AI boom isn’t just a Big Tech story anymore. It’s vertically and horizontally integrated into nearly every corner of the economy one way or another. 📌 Bottom line: Whether this is the 1995 or 1999 phase of the AI boom, it’s already redrawing the U.S. economy in ways that will last for years for better or worse. | | | | 🎭 Will small caps take the charge from here? | | | | Small-cap stocks have been quietly rallying alongside their megacap counterparts, pushing the Russell 2000 near record highs to close out last month. 📌 Wall Street hunts for value The enthusiasm around small caps makes sense, at least by the textbook. Valuations look cheap compared to large caps, the margin for error is smaller since many are trading below historical valuations, and earnings growth projections are higher. A few quick stats: -

The Russell 2000 has outpaced the S&P 500 since April, lifted by rate-cut hopes -

Small caps are expected to deliver more than double the profit growth of large caps -

The small-cap index’s share of the Russell 3000 sits at just 4.4%, far below its long-term average of 7.6% Royce Investment Partners’ Francis Gannon noted that investment strategists see them as a contrarian play in a Big-Tech-dominated market. “Consumers continue to spend, the economy is growing, and access to capital has widened,” he said. ⚠️ The profit problem Beneath that optimism lies something of a conundrum. Unprofitable small caps have surged twice as fast as profitable ones, up 19% versus 9% this year, according to Lazard’s Oren Shiran.

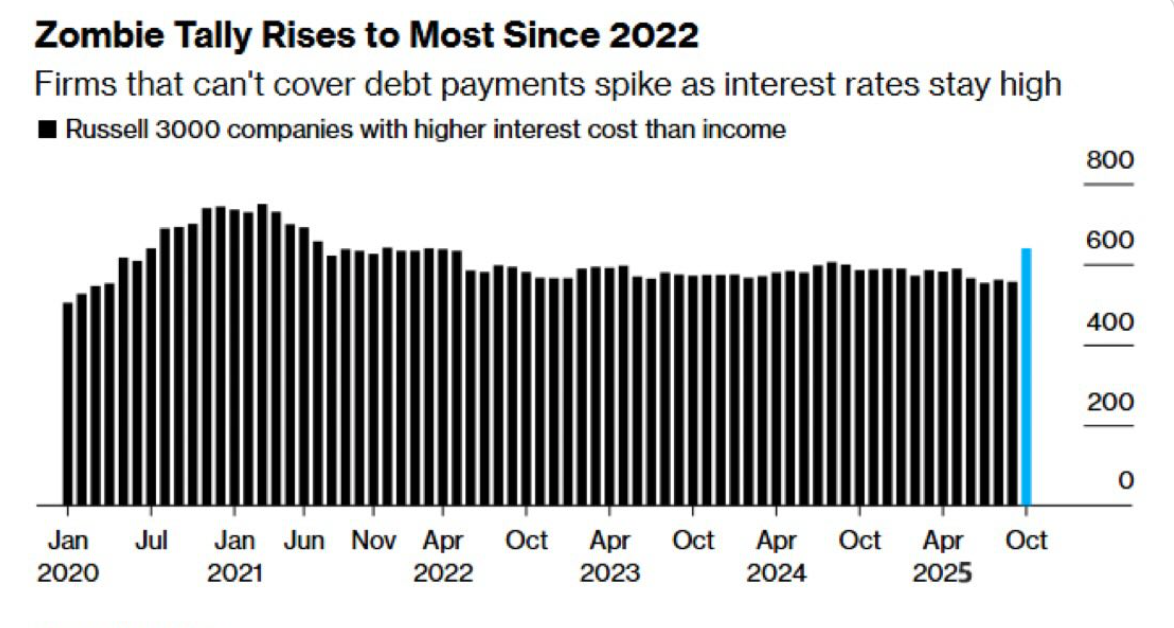

So for now, both large and small caps share the same existential question: How long can price growth outrun profit growth in this cycle? But if history is any guide (and the Fed follows through with more rate cuts) small caps may fare better. After the 2001 and 2008 rate-cutting cycles, small caps (Russell 2000) generally outpaced the S&P 500 in the six- to twelve-month window following the first cut. That’s assuming the Fed stays ahead of the curve and prevents a recession. | | | | 🧟 Halloween over, but zombies aren't | | | | Debt isn’t just a problem for the federal government and households. It’s also becoming a major concern on Wall Street... The so-called zombie companies (businesses that don’t make enough profit to pay the interest on their debt) are springing up at the fastest pace in years. 📊 By the numbers -

Nearly 100 new zombie companies emerged in October, according to Bloomberg data -

That’s the biggest month-over-month increase since early 2022 -

Many of the new entrants are in the once-hot biotech and healthcare sectors Among the debt-laden names now stumbling are Altice USA (ATUS), whose 2029 bonds trade below $0.80 on the dollarm, and Tronox Holdings (TROX), whose new notes have already dropped about $0.09 since issue. Lionsgate Studios (LION) is another notable member of the zombie club, hit by higher costs, trade turmoil, and shrinking subsidies. 💬 What analysts are saying Companies that took out debt like there was no tomorrow when money was cheap are now having trouble paying it off or refinancing. Charles Schwab chief investment strategist Liz Ann Sonders noted that debt piled up during the zero-rate era “now looks untenable.” Borrowing costs remain “higher than historic averages,” she wrote, adding that even if the Fed keeps cutting, most of these firms “were barely scraping by at zero.” For many zombie companies, the problem isn’t just higher rates. It’s their entire balance sheet design. As Oaktree Capital’s David Rosenberg put it, “these balance sheets were structured when rates were low, and they don’t necessarily work when rates are high.” Shannon Ward of Capital Group flagged earnings erosion and maturity risk as another red flag. With S&P Global already cutting earnings forecasts across the homebuilding, energy, and chemicals sectors, refinancing options are vanishing fast. “There is more distress in the market than participants will admit,” warned King & Spalding’s Carolyn Alford. 📌 Bottom line: The Halloween costumes might be gone, but zombies are still roaming up and down Wall Street, and they’re multiplying. | | | | Rate today's newsletter*... | | | * We are just a messenger. To avoid confusion, please rate the quality of reporting, not news | | | | | | | | | | | | InvestorsObserver | | You received this email because you signed up on our website or made a purchase from us. | | | | |