There will be drama when the markets open in New YorkStocks are selling off globally this morning as unhappy investors see the price oil rising again—because of renewed conflict in the Middle East—and President Trump’s

inability to rein in Israeli Prime Minister Benjamin Netanyahu. There’s also a total meltdown in semiconductor stocks—a bad sign for the SpaceX IPO on Friday. The VIX fear index is up 24% over the last five days. “There seems to be no single cause, rather a general sense of increasing risk,” UBS’s Paul Donovan said this morning.

- The S&P 500 declined 2.64% on Friday, a huge drop. The tech-heavy Nasdaq was even worse, down 4.18%. The Philadelphia semiconductor collapsed 10.26%. This morning, S&P futures rose 0.35% prior to the opening bell—perhaps suggesting that retail investors might once again step in to buy the dip.

- Brent crude was $97 per barrel this morning, up sharply on news that Iran and Israel had resumed bombing each other.

- In Europe, the Stoxx 600 was down 0.75% in early trading and the U.K.’s FTSE 100 was down 0.4% before lunch.

- Asia: South Korea’s KOSPI down an astonishing 8.29%. Japan’s Nikkei 225 was down 3.85%. India’s Nifty 50 was down 0.9%. China’s CSI 300 was down 2.14%.

- Bitcoin was $63K.

Investors are still trying to digest Friday’s surprisingly strong U.S. job numbers, the question of

whether the Fed will spoil all the fun by raising interest rates, and

the bubbly prospect of three huge IPOs in the AI sector, coming this year.

One thing is for sure: stock buyers sent a strong warning to the market that their patience is not limitless. They may have turned a blind eye to trade tariffs and the high price of oil until now, but they’re not going to ignore rising interest rates and low-quality AI financials.

What traders appear to be thinking is that the robust jobs number—payrolls rose 172,000 in May, far above expectations of around 88,000—will persuade the Fed that the economy is running hot, especially if inflation (currently 3.8%) moves up toward the unemployment rate (4.3%). A new consumer price index number will come out on Wednesday.

Most Wall Street analysts now say that any further Fed interest rate cuts are off the table, and many predict the central bank will raise interest rates later this year. That’s bad for stocks, because it makes new money more expensive—hence Friday’s massacre.

It’s bad for bonds too, because higher interest rates make debt more expensive. That’s where the link to AI and tech stocks comes in. Google issued $85 billion in new stock last week and

Meta is considering doing something similar. That came after both Meta and Oracle raised billions in private debt to fund AI data center buildouts. “Hyperscaler supply [of new debt] has reached $159 billion year-to-date, which is 91% of our $175 billion forecast for the full year,” Bank of America’s Yuri Seliger told clients recently. It was roughly $121 billion last year.

“We didn’t see this coming”Economists were shocked by the jobs number on Friday. (Vanguard, for instance,

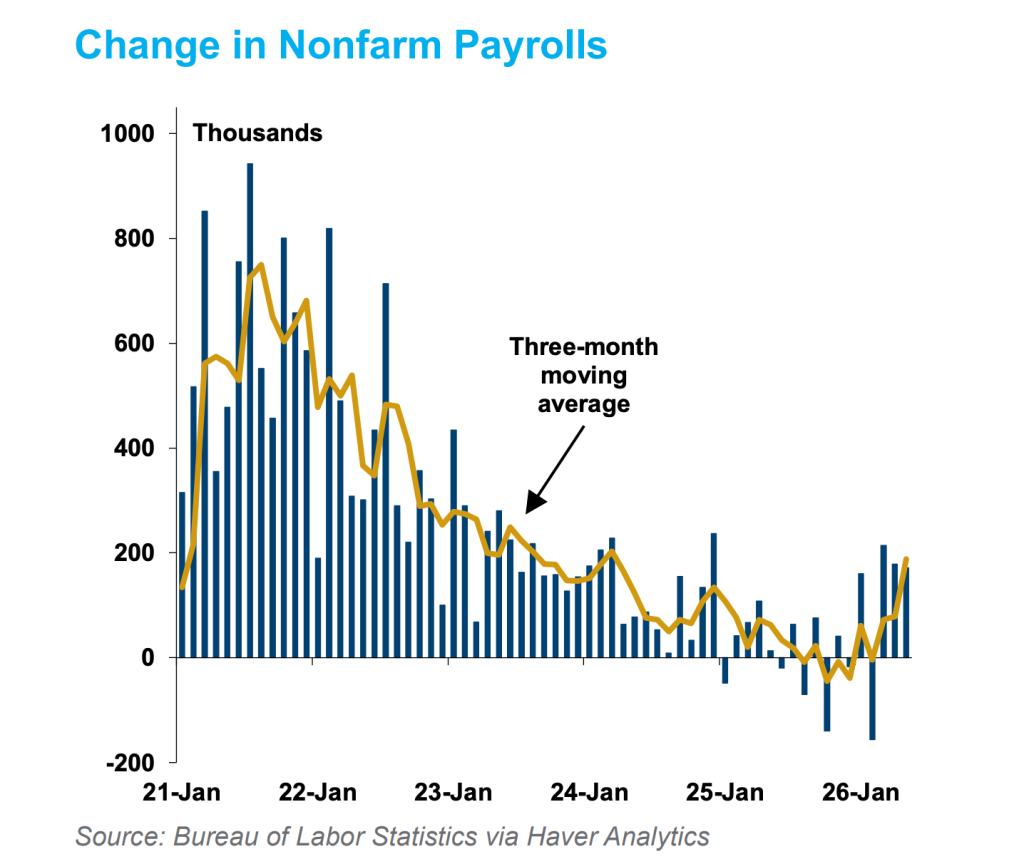

forecast a gain of only 20,000 jobs.) “We didn’t see this coming,” Pantheon’s Samuel Tombs and Oliver Allen said in a hastily written email. “Payrolls have surprised the consensus to the upside for three straight months, a relatively rare occurrence which suggests the improvement is more than just noise ... the three-month average of private payrolls has picked up to 166K—its highest since June 2023—from 8K in February.”

This chart from Daiwa Capital Markets shows that the job market now appears to be in an upswing. Before the revisions, it looked rather flat:

Growth, yes, but it’s narrow and fragile

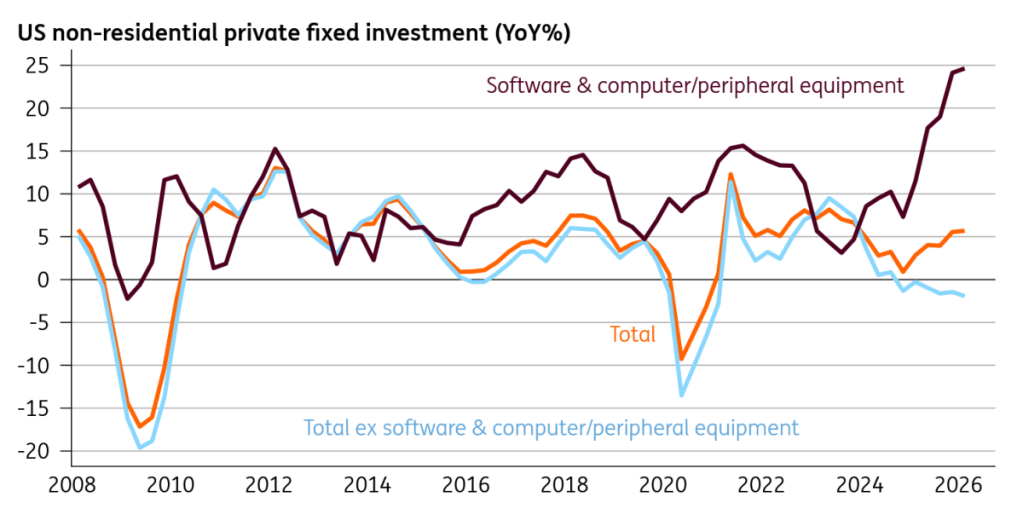

Growth, yes, but it’s narrow and fragileWhile that economic growth is nice, it also looks very narrow. All U.S. growth in private, non-real estate, investment is in decline—except for AI, as

this chart from ING’s James Smith shows:

“The circularity [of the AI economy] is attracting more attention: the same handful of firms raising money, buying chips, leasing compute, and booking revenues off one another. That may not spell disaster,” he says “but the fact remains that if you strip out AI, the rest of U.S. private non-residential investment has been falling year-on-year for six straight quarters.”

And all the job gains came from just three sectors: leisure & hospitality, government, and private education and healthcare services. Only 10,000 other jobs were created outside those sectors,

ING’s James Knightley noted. So there’s growth—but it is highly concentrated in just a few areas. “While this is a very good report at the headline level, the lack of breadth to the job creation story remains an important theme,” he says.

SpaceX IPO on Friday will be a huge testAt the same time, SpaceX, Anthropic, and OpenAI are all expected to go public this year. They are all AI companies (SpaceX contains the Grok AI model). SpaceX—which will launch its IPO on Friday—is not profitable and the other two are not expected to be, either. It’s not at all clear whether investors will welcome the excitement of these megacap companies or reject them

as money-losing bubble stocks.

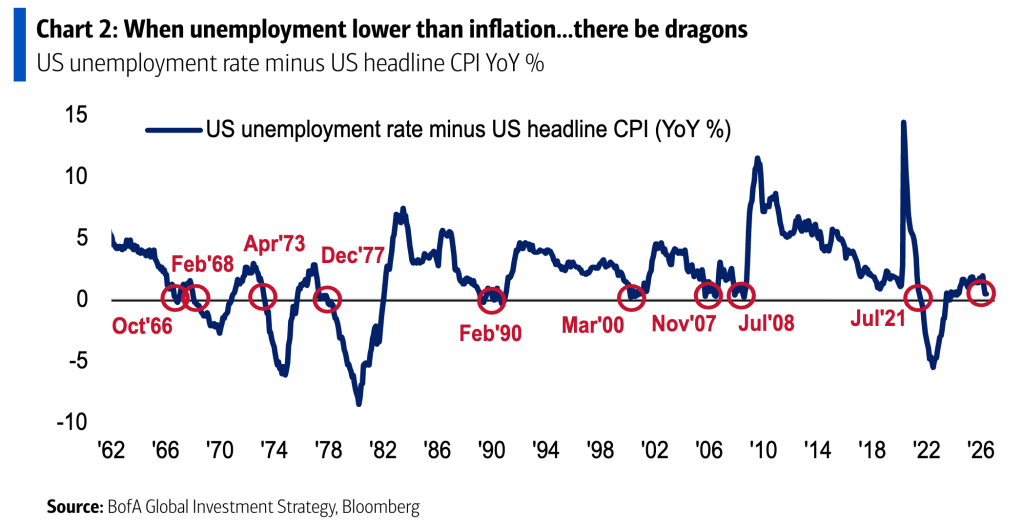

“There be dragons”Finally, Michael Hartnett and his colleagues at Bank of America pointed out in a note seen by

Fortune that this week there is a chance the headline inflation rate could go

above the unemployment rate—which is almost never good. If that happens, it would be only the seventh time since 1960. Those years ('66, '73, '90, '00, '08, and '21) featured “years of Fed hikes, and none remembered well on Wall Street,” he says. He also noted that the unemployment rate minus consumer price inflation “has [a] strong correlation with U.S. yield curve, and points to inversion.” Yield curve inversion—when investors become more afraid of the near-future than the long-term—is a traditional harbinger of recession.